Delta bought $1Bn+ of their own shares in February 2019. In doing so, Delta accelerated management’s planned capital return to shareholders. My first thought was “Delta thinks its stock is cheap.” Today, I view the move as smart capital allocation with potential upside.

Delta funded the transaction with a seasonal working capital debt facility. Usually a company has to pay an upfront fee to obtain a new debt facility. Let’s assume the upfront fee was ~37.5bps given Delta’s credit profile and ongoing bank relationships. Like all debt facilities, there’s an associated interest expense with the facility. These facilities are usually priced in relation to LIBOR. For this discussion, I assumed Delta has to pay LIBOR + 150bps. That said, I suspect the cost is closer to LIBOR + 75bps or LIBOR + 100bps. Either way, the example yields the same conclusion.

Assuming Delta obtained the facility in January, the cost of the facility looks something like this:

As shown above, Delta incurred an incremental interest expense of roughly $13.8mm. What did Delta gain?

Delta’s dividend savings during the period almost exceeded the cost of the facility. On an annualized basis, the dividend savings exceed the assumed facility cost by 138%. Obviously, this math can get taken to an extreme because the company can retire more shares as it borrows more money. That said, this is a great example of how an investment grade balance sheet enables a company to play offense when opportunities present themselves.

Delta’s decision carries some risk. If the summer travel season is poor then Delta may not be able to pay the facility off as quickly as I assume. In that case, the facility costs will exceed my projections. Nevertheless, the company could manage an additional billion dollars of debt, if necessary (it had $1.9Bn of cash as of 3/31/19).

Importantly, despite any temptations, management didn’t get too carried away on the facility size. Accordingly, Delta made a low risk, potentially high reward bet. Those are exactly the kinds of bets I want my management teams making.

NOTE: Delta increased their dividend from $1.24/sh/yr to $1.40/sh/yr following the repurchase. This reduced the annualized savings from retiring the February shares from $24.3mm to $2.2mm. Personally, I would prefer for them to retire the shares and pay special dividends rather than raising the promised dividend. That said, I understand management’s decision and remain pleased with the corporate finance decisions.

It doesn’t make any sense that Warren Buffett, arguably the greatest quality investor ever, retreated to his “value” roots to invest in airlines. This is the same guy that didn’t let Nike get through his investment filter. And now he invested in airlines? Airlines! The…worst…business…ever. Or is it?

Note: This is not investment advice! An airline investment is extremely risky and should only be undertaken after deep due diligence. If you believe what is written here and buy the shares of any company mentioned you should expect to lose your capital to someone more informed than you. Furthermore, the volatility in airline stocks is not for the faint of heart. Do not let yourself get interested in this idea if you consider Beta to be a meaningful metric.

Airlines: A Brief History

First, some facts must be stated:

Airlines will never be a capital light business. They require reinvestment to remain relevant. They may not need to purchase all new airplanes (ahem, American), but they do have to consistently reinvest in the cabin and airport experience.

No matter what, people will complain about flying. Very rarely do you hear someone say “Let me tell you how much I enjoy flying commercial airlines.” Usually people say they are being treated like cattle and getting gouged. The gouging claim is particularly interesting considering its never been less expensive to fly, but I digress. See https://www.travelandleisure.com/airlines-airports/history-of-flight-costs

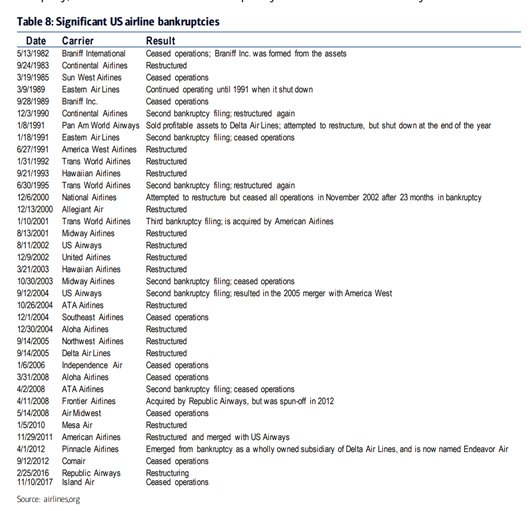

The history of the airline industry is littered with wasted stakeholder capital. Note, I did not say shareholder. Everyone has had to compromise; shareholders, debt holders, employees, and sometimes customers. Here’s a quick look at a truly horrendous industry history:

Source: BAML

Historically, financially weak competitors wreaked havoc on financially responsible airlines. Usually, the weak competitor had poor cost structures and too much leverage. Combine that with high exit barriers and high fixed costs and you have a recipe for disaster.

Why? Airline seats are commodities. Always have been and probably always will be. Thus, airlines can’t do much when competitors react to financial trouble by pricing seats to cover variable (rather than all in) costs. Once an airline prices seats in that manner, all competing airlines are faced with two bad choices:

Don’t match price, lose yield, and pray to cover costs.

Match price, lose margin, and pray to cover costs.

Neither of those choices are great. The problem gets exacerbated when the financially distressed competitor files for bankruptcy. Bankruptcy usually enables poorly run/capitalized airlines to restructure their liabilities (such as union contracts, debt arrangements, etc.). Following the bankruptcy proceedings, a new, lean airline emerges to compete against the well run and responsible airline. Thus, responsible airlines have had to compete with poorly run airlines while they were in decline followed by cost advantaged competitors post restructuring. That’s a tough equation.

The Enigma

If all that is true why did Buffett choose to invest in this space? Doesn’t he understand history? Doesn’t he understand that buying a one of a kind brand like Disney at a market multiple is a great bet? Isn’t he the one that said a capitalist should have shot the Wright brothers? Isn’t this the man that said:

“Businesses in industries with both substantial overcapacity and a ‘commodity’ product are prime candidates for profit troubles. Over-capacity may eventually self-correct, either as capacity shrinks or demand expands. Unfortunately for the participants, such corrections often are long delayed. When they finally occur, the rebound to prosperity frequently produces a pervasive enthusiasm for expansion that, within a few years, again creates over capacity and a new profitless environment.”

The Pari-Mutuel System

Buffett understands compounders, capital light compounders, pricing power, quality, and any other phrase you throw at him. But, what I believe he understands better than most is the odds at which each bet stacks up against each other. As Charlie put it:

“Any damn fool can see that a horse carrying a light weight with a wonderful win rate and a good post position etc., etc. is way more likely to win than a horse with a terrible record and extra weight and so on and so on. But if you look at the odds, the bad horse pays 100 to 1, whereas the good horse pays 3 to 2. Then it’s not clear which is statistically the best bet…The prices [are such]…that it’s very hard to beat the system.” – Charles T. Munger

While the odds offered are important, any damn fool can also tell you a three legged horse isn’t going to win the race. A lame horse is a lame horse. Good odds aren’t going to change that. So, what does Warren see that makes this horse worth betting on?

Industry Facts

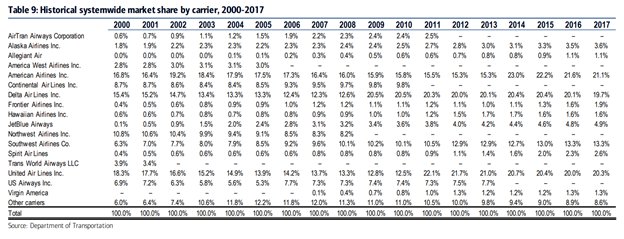

Today, 4 major airlines control 80+% of all US seats.

Source: BAML

More importantly, at least 3 of the 4 are financially stable. The one that concerns me the most is American. Doug Parker, American’s CEO, would respond by saying the company’s loan to asset value (“LTV”) is reasonable. I don’t necessary disagree with that thought process. However, I worry about the interest expense (an added fixed cost in a downturn) causing irrational behavior. Given the industry’s history, I’d far prefer American to have a better balance sheet this late in a cycle.

Nevertheless, here is Scott Kirby, President of United, discussing what is “different this time:”

American remains my “canary in the coal mine.” That said, American is acting rational and the Big 4 have been rational since they consolidated. Whether they remain rational in a downturn remains TBD. But, as my friend Jake Taylor mentioned in his book The Rebel Allocator, industries can usually remain rational when they have under 5 major participants…

In the meantime, airlines benefit from:

structural tailwinds (people valuing travel and bragging via Instagram; the trend towards urbanization also helps because consumer spending on travel to see family has proven to be resilient),

technological advancements (far better scheduling and pricing ability),

more efficient, rolling hubs (3 large legacy carriers can run much more efficient hubs than 6 carriers could ever hope to),

decoupling of booking fees and ancillary revenues (ancillary revenues are harder to price shop and therefore more inelastic),

airport infrastructure that is difficult to expand (gates are somewhat constrained), and

the often overlooked credit card agreements.

A Quick Note on Game Theory

Airlines seem to face a prisoner’s dilemma with pricing decisions. A description of the prisoner’s dilemma can be found at https://en.wikipedia.org/wiki/Prisoner%27s_dilemma. There’s validity to the argument that in any given pricing situation Airline A is incentivized to “cheat” on price in order to gain market share. Since Airline B is afraid of that incentive, Airline B is incentivized to do the same. Thus, they will both end up cheating and aggregate returns will be suboptimal.

However, the prisoner’s dilemma applies to a game played only once. In the airline industry the game is played thousands of times every day. If Airline A cheats on one route, Airline B can respond on a different route. The 4 major participants signal to each other over and over again. They all also respond to these signals. When the game is repeated with such frequency it’s more likely to lead to prices that generate acceptable (though not great) returns.

Therefore, the repetition of the game reduces the potentially destructive incentives to cheat. Borrowing/bending a term from physics, the industry remains in quasi stable equilibrium. See

Competitive Position Assessment

SCG likes the competitive positions of the ultra low cost carriers (Allegiant, Spirit, Frontier), Delta (generates a revenue premium), and Alaska (benefits from a cost advantaged union contract that is unlikely to go away). As I see it, costs are the only way to win consistently in commodity industries. That said, Delta is an incredibly well run airline and has proven revenue premiums are sustainable in this industry. It’s only right to credit Phil Ordway of Anabatic Investment Partners as the original source for that line of thought. His thought process is compelling and I haven’t been able to debunk the reasoning. Disclaimer: Long Delta and Alaska.

Credit Card Agreements: The GemNo One Cares About

The industry’s credit card agreements are immensely profitable for the airlines. Further, the cash flows are growing at reasonable rates and generate free cash flow “float.” Alaska Air Group discussed their credit card agreement at a JP Morgan event. Here’s what they said:

Note: ALK’s enterprise value is $11.4Bn (inclusive of pension obligations and operating leases). So, cash flow from credit card/loyalty agreements totals 8.7% of a fully baked enterprise value.

It’s certainly interesting that Buffett, who’s core competence is financials, just happens to be interested in airline stocks at the same time the industry’s credit card economics improved. Maybe it’s a coincidence. Maybe not.

At a minimum these credit card agreements are a very efficient way to finance the business. A bull would argue this portion of the business is a high margin sales organization growing at ~14% per year. What’s that worth? Joe DiNardi, an analyst for Stifel, Nicohaus & Co is asking that same question:

Most importantly, why have the credit card economics changed so much and are these changes sustainable? That was a difficult question to answer. Scott Kirby believes it’s because of the airlines’ improved financial positions. See below:

Mr. Kirby’s explanation is rational. Distressed loans require banks to hold more capital against the loans. That additional capital requires a return. Therefore, the notion that banks historically hit their “hurdle rate” by keeping all the credit card economics makes sense. With the industry in better shape, banks now hold less capital against the loans and probably generate more cash management (and other ancillary) revenues. Thus, they are more willing to give up some of the credit card economics.

Importantly, Delta’s recent announcement seems to suggest the good times will continue for the airlines and credit card commissions. That’s good for all stakeholders.

Why Delta

Now that we’ve established that airlines might be reasonably healthy horses, it’s time to look at the odds offered on the bet. This post will analyze Delta because SCG believes it’s far and away the best run hub and spoke airline in the world. Further, Atlanta is a sustainable competitive advantage for Delta’s network. Atlanta is so valuable because it’s incredibly efficient. Some estimates say Atlanta is up to 200bps more profitable than other hubs. This advantage stems from Delta dominating the hub and Atlanta’s traffic volume.

Perhaps most importantly, Delta can survive turbulent periods. In the event of a downturn, Delta has $1.9Bn of cash, $3.0Bn of revolver availability, and generated free cash flow in 2009. Therefore, Delta can probably handle the left tail of potential outcomes. Delta has $1.7Bn of debt maturities coming due in 2020 and $1.4Bn due in 2022. It would be nice to see them refinance and meaningfully extend the term of that debt. Now is a good time to refinance because debt markets are seemingly starved for yield.

Delta’s Offered Odds

With that in mind, let’s take a look at Delta’s free cash flows available to equity since 2009. This analysis of free cash flow available to equity adds back a proformaadjustment assuming 40% of capex was financed with debt. As of today, Delta’s debt to Net PP&E totals 37%. Delta’s management is pleased with the balance sheet today. Thus, analyzing average free cash flows using a proforma adjustment assuming 40% of capex will be financed going forward is reasonable assumption.

Since 2013, Delta’s average pro forma free cash flow available to equity totaled $4.1Bn per year. As stated, this number rests on the proforma adjustment assuming that 40% of capex was/will be financed. Again, I am comfortable with that assumption because (a) it’s unreasonable to expect Delta to not finance any equipment purchases, (b) the balance sheet is in a reasonable financial position (debt and debt like obligations account for 41% of asset value; those obligations consist of $9.0Bn of pension obligations, $10.7Bn of debt, and $5.8Bn of operating leases), and (c) it’s more important to figure out how the business is going to look going forward rather than what it looked like in the past.

2013 is a valid starting point for the analysis because it is the year the DOJ approved the last of the Big 4 mergers. A reasonable argument can be made that requires the analysis to look back to 2009 (which is why I showed those years as well in the chart above). That said, I base this analysis on the competitive period that is most similar to today.

Going forward, Delta should return most of the free cash flow available to equity to shareholders. Let’s say they use 20% of cash flow to build cash reserves and 20% to voluntarily reduce pension obligations. That leaves about $2.5Bn for dividends and share repurchases. As of 3/31/2019 there were 655mm shares outstanding with a promised dividend of $1.40/share/year. Therefore, Delta will be paying roughly $920mm in dividends annually. Thus, approximately $1.5Bn, or 4% of the current market cap is available for share repurchases. Note, this assumption doesn’t take into account the impending growth in credit card cash flows.

I’d be remiss not to mention that Delta’s market cap includes $2.0Bn of equity investments in other airlines, a refinery that does about $4.0Bn of sales every year (total assets were $1.5Bn at 3/31/19), and a maintenance repair organization (“MRO”). The MRO has run rate revenues of ~$800mm annually with “mid teens” margins. Further, Delta expects the MRO to achieve $2Bn of revenues over the next 5 years. All together lets say the assets mentioned in this paragraph are worth $4.0Bn.

Accepting the assumptions above, Delta currently trades at an 11+% free cash flow available to equity yield. Moreover, they have the opportunity to “buy in” 4% of their shares every year. IF the competition remains rational shareholders have a reasonable chance to earn 13-15% on their capital in the foreseeable future. Those kinds of returns will generate a lot of wealth when rates are below 3%.

The Bet

Returning to Munger for a moment…the airline “horse” may not be the best. But the odds offered are intriguing. Importantly, the horse is reasonably healthy. One question remains: is the future actually different this time? Who knows? Buffett put his chips in. I did too. But, I may be some schmuck that convinced himself an elegant theory was correct because I wanted to believe it so badly. Time will tell. I’ll still be in the position when the story is told.

The beauty of this game is Buffett’s “fat pitch” doesn’t have to be anyone else’s. Regardless of people’s conclusions, it’s important to look at why the greats do what they do. The thesis above isn’t dispositive, but it does hit many of the key points. See also

for a bit more industry information.

As always, please feel free to contact me with any questions and/or corrections.

PS. I asked Charlie about the airline investment. He said this:

And really any of the speeches at The Wings Club found on YouTube

The Rebel Allocator is a fantastic and fun book with many pearls of investment wisdom.

PPS. If you liked any of the above commentary look into subscribing to Airline Weekly. Also, follow Phil Ordway @pcordway on Twitter. Phil is the Portfolio Manager at Anabatic Investment Partners LLC. He gave a fantastic presentation to Manual of Ideas that started my research journey. Finally, try to participate in any Manual of Ideas events you can. John Mihaljevic puts on great events and strikes me as a person doing it for the right reasons.